By Thomas Wells, fund manager, Sanlam Investments

As a short and honest response to this question, the juiciest opportunity in inflation-linked bonds is probably behind us, but it is not too late for those who have yet to jump aboard. Continuing the nautical analogy, it is worth remembering that the global economy is a super tanker and not a yacht! It will take a long time for the macro picture to become clear and even longer for the authorities’ response to inflation to take effect. Remember that monetary policy works with a lag, some nine to twelve months usually. We’ve outlined our thoughts below.

What is priced in?

Inflation fears have shifted nominal yield curves higher across the developed world. If we strip out the current extra dose of volatility from Russia and Ukraine, there are roughly 6 hikes of 25bps priced into the US rates markets this year. In Europe, where the outlook remains very different, the market has priced in at total of 40bps of tightening from the Central Bank by the end of 2022.

How do we calculate performance of inflation-linked markets against nominal bonds? One way to measure this is the difference in yield between the two markets, namely the breakeven rate. Let’s examine this in a bit more detail:

Source of all data: Bloomberg, 22 February 2022

Past performance is not a guide to future performance

The red line shows the 10 year US government bond yield (the nominal bond yield), currently off its highs at 1.95%

The blue line shows the 10 year US government real yield, currently around -0.51%

The black line shows the difference - the Breakeven rate - at 2.46%

Think of the black line as the market’s assessment or best (educated) guess of what annualised inflation will turn out to be over the next 10 years.

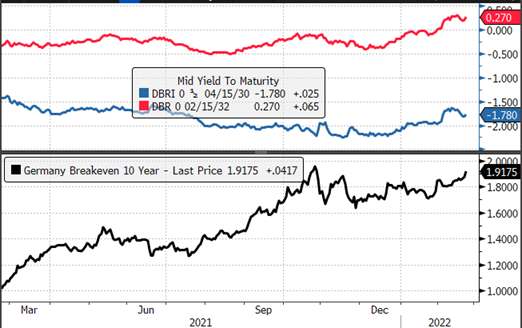

For Europe we have shown the core government bond market, the German market, below. The European market has not priced in as much inflation over the next decade and in fact prices in less than the central bank target:

Source of all data: Bloomberg, 22 February 2022

Past performance is not a guide to future performance

Is any of this important?

We believe that the outlook for inflation and the consequent reaction from the Fed, European Central Bank and the Bank of England is the most important question facing investors today and will determine the path for bond markets (as well as equity markets) throughout the rest of 2022 and potentially into 2023. Clients often ask what might happen over the next six or twelve months but we have to provide a caveat: we don’t know the exact path inflation will take over that time. Nonetheless, we can make the following observations about the backdrop:

- Inflation will be fought by tightening rates and we have already priced in a significant tightening in the rates markets

- A well-diversified portfolio is the best way to proceed while uncertainty is so high

- Duration has proven time and time again to be the best hedge against unknowns such as Covid and the Russia/Ukraine escalations – when the chips are down, you want your bond holdings to perform like bonds

Bringing it all together

The US central bank targets the core Personal Consumption Expenditures (PCE) inflation rate, which rose by 4.9% in December compared to the prior year. The ‘headline’ inflation rate that we observe in the market is much higher at 7.5% year on year in January 2022. The point is that for the Fed, the inflation rate is not as awful as it might appear to the Biden administration, and this point adds a fair bit of extra complexity to the outlook. It is also interesting in that the targeted inflation level is not as bad as the headline suggests. Finally, on this point, the US inflation-linked bonds that we invest in are linked to Consumer Prices Index (CPI), whereas the Fed is attempting to control PCE. This gives the bond holders a nice cushion (due to the materially higher inflation levels seen with CPI).

The outlook for growth in the developed world is deteriorating, i.e. economies are still seeing some expansion, but at a much lower level than previously anticipated. This means that tightening rates to further slow the economy while consumers are beginning to feel the pain of inflation in their pockets is not as easy as the central banks might like. Tightening more aggressively than the market has priced in would slow the economy further and thus bring about the threat of a recession faster. The ideal solution for central banks here is that inflation slows slightly, enabling them to deliver a gentle tightening cycle which doesn’t bring about a recession and consequently leaves the growth picture in healthy shape. That is also a great solution for the markets.

The final thing to mention is that there are a number of inflationary forces at work globally and if one were to draw a probability distribution curve with the centre of that distribution being the current expectation for 10-year inflation to be the market-derived figure of 2.46%, then we would suggest there is a ‘fatter’ right-hand tail (that is, a higher probability of inflation outcomes being higher than 2.46% over the next decade) than lower. This point is the reason why we believe it’s important to maintain exposure to the asset class. As the globe copes with deglobalisation, the huge costs of decarbonisation, upward adjustments to wages, the higher housing costs that we are seeing across the developed world, and of course higher gas prices due to conflict in key geopolitical areas, the impacts are likely to be seen on the right-hand side of that probability distribution curve, and consequently holding assets linked to that is probably a good hedge and could form part of a portfolio, in our view.

In addition, we mentioned that duration has proven to be a good hedge against unforeseen events. The problem is that nominal duration carries too great a risk as there is absolutely no protection from rising inflation, so duration is better taken with the inflation linkage offered by ‘real’ bonds. Moreover, credit, particularly at the riskier end of the spectrum, has shown a tendency to widen out recently and consequently underperform government debt. We don’t believe that this will continue for long, but it is an additional risk that our fund (Sanlam International Inflation-Linked Bond Fund) seeks to mitigate.

In short, we believe hedging out inflation risks is a good idea. Our fund diversifies exposure across the developed world by capturing the upside across a range of inflation measures. We do not believe that we are suddenly going to see an end to inflation as the anniversary effects reduce the year-over-year numbers. Putting it another way: if the market has only priced in 2.46% inflation in the US and 1.91% inflation in Germany, we think there is still value left on the table – International inflation-linked bonds are still worthy of consideration.

Important information

This document is marketing material for professional investors only. Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital.

Issued and approved by Sanlam Investments which is authorised and regulated by the Financial Conduct Authority. Sanlam Investments is the trading name for our two Financial Conduct Authority (FCA) regulated entities: Sanlam Investments UK Limited (FRN 459237) and Sanlam Private Investments (UK) Ltd (FRN 122588), both having its registered office at 24 Monument Street, London, EC3R 8AJ. The UCITS Management Company has the right to terminate the arrangements made for the marketing of funds in accordance with the UCITS Directive.

The opinions are those of the author at the time of publication and are subject to change, without notice, at any time due to changes in market or economic conditions. Whilst care has been taken in compiling the content of this document, neither Sanlam nor any other person makes any guarantee, representation or warranty, express or implied as to its accuracy, completeness or fairness of the information and opinions contained in this document, which has been prepared in good faith, and to the fullest extent permissible under UK law.

Some parts/sections of this document may have been compiled from external sources. Whilst these sources are believed to be reliable, the information has not been independently verified and is subject to material amendment, revision and updating, therefore no representation is made as to its accuracy or completeness. No reliance may be placed for any purpose whatsoever on the information, representations or opinions contained in this document nor shall it or any part of it form the basis of or act as an inducement to enter into any contract for any securities, and to the fullest extent permissible under UK law no liability is accepted or any such information, representations or opinions. The comments should not be construed as a recommendation of individual holdings or market sectors, but as an illustration of broader themes.

Statements in this document that reflect projections or expectations of future financial or economic performance of a strategy, or of markets in general, and statements of any Sanlam strategies’ plans and objectives for future operations are forward-looking statements. Actual results or events may differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statement. Important factors that could result in such differences, in addition to the other factors noted with forward-looking statements, include general economic conditions such as inflation, recession and interest rates, political or business conditions or in the tax or regulatory framework in the UK or other relevant jurisdictions, any of which could cause actual results to vary materially from the future results implied in such forward-looking statements. No assurance can be given as to the future results that will be achieved.

Sanlam makes no representation as to whether any illustration/example mentioned in this document is now or was ever held in any Sanlam Fund or Model Portfolio. Examples / Illustrations shown are only for the limited purpose of analysing general market, economic conditions or highlighting specific elements of the research process.