Peter Doherty, Head of fixed income

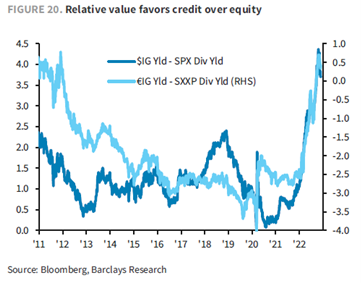

Attractive entry point for selective parts of the credit markets

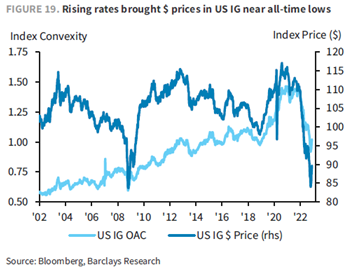

Total returns should be robust: Returns were abysmal for credit in 2022, with the rate moves the largest factor.

Starting levels are much more attractive from a yield standpoint and provide room for error, whether it is spread widening in a recession or a rise in downgrades and defaults

Expect higher frequency of defaults and idiosyncratic risks in Corporate Bonds and Leveraged Finance

Allianz Trade anticipates 36% increase in insolvencies in Italy in 2023, followed by France (29%), Germany (17%) and the UK (10%). In China, the company expects 15% more insolvencies on the back of lower growth and a limited impact from monetary and fiscal easing. In the US, it anticipates an increase of 38% on the back of tighter monetary and financial conditions. It gives three main reasons for the expected increase in insolvencies: 1. The major profitability shock for European firms due to the energy crisis, 2. The interest rate shock and higher wage bill due to a sharp increase in inflation, and 3. Only limited intervention expected from governments.

For US High Yield amid a challenging macro environment, risk assets will face further pressure next year, though spreads should peak in the first half and recover somewhat by year-end resulting in total returns of 4.0-5.0%.

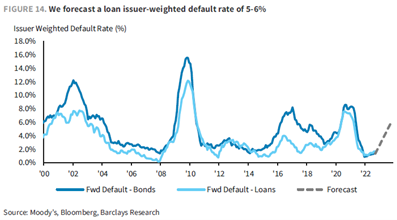

Default rates in high yield and loans to end 2023 at 5.0-6.0% on an issuer-weighted basis. Though they have remained near historically low levels post-COVID, there are many factors pointing to higher default rates next year.

Impact of 2022 Central Bank rate increases to be felt across Private Equity, Private Credit and Real Estate valuations

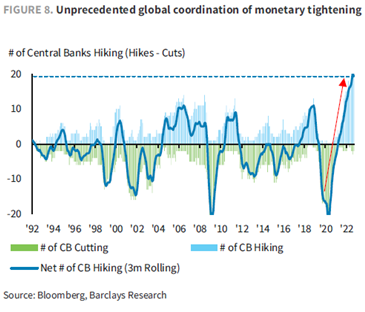

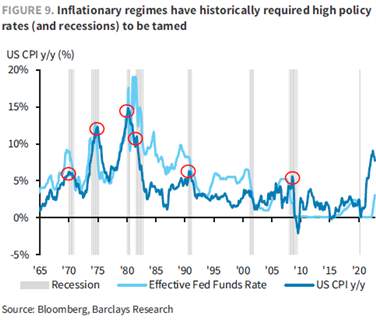

Corporate fundamentals will be challenged by slowing growth globally, with a recession in the developed economies. This will create a tough operating environment for corporates. Furthermore, US non-financial revenue growth is more correlated to European GDP now than pre-GFC. We believe that corporate fundamentals will continue to deteriorate in an adverse operating environment.

Remain invested in high quality, investment grade companies which can sell assets, reduce headcount, and raise equity long before asking bondholders to share losses.

Pick up additional yield by investing down the capital structure into Tier 1 / Tier 2 Bank and Insurance Hybrid Capital

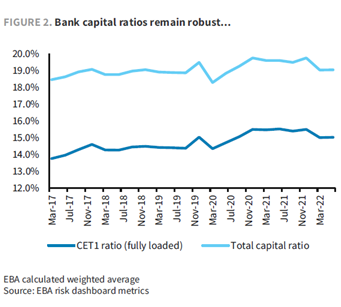

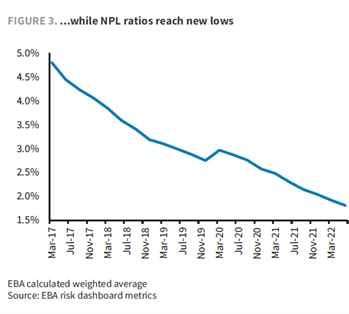

US, EU and UK Bank and Insurance company balance sheets will come under some pressure as asset quality and values deteriorate but current excess capital and robust risk management offer a substantial cushion. With insolvencies set to increase next year in a potential recession, European banks are likely to experience an increase in impairments.

Higher impairments should be broadly manageable for most banks, provided the unemployment rate does not spike up dramatically. This is due to banks having decent starting capital positions, strong asset quality metrics and some existing impairment overlays put in place for the COVID pandemic.

Source: All charts supplied by Barclays Credit Research, December 2022.

Important information

This document is marketing material.

Issued and approved by Sanlam Investments which is authorised and regulated by the Financial Conduct Authority. Sanlam Investments is the trading name for Sanlam Investments UK Limited (FRN 459237), having its registered office at 24 Monument Street, London, EC3R 8AJ. The UCITS Management Company has the right to terminate the arrangements made for the marketing of funds in accordance with the UCITS Directive.

The information contained in this document is for guidance only and does not constitute financial advice

The opinions are those of the author at the time of publication and are subject to change, without notice, at any time due to changes in market or economic conditions. Whilst care has been taken in compiling the content of this document, neither Sanlam nor any other person makes any guarantee, representation or warranty, express or implied as to its accuracy, completeness or fairness of the information and opinions contained in this document, which has been prepared in good faith, and to the fullest extent permissible under UK law. Some parts/sections of this document may been compiled from external sources. Whilst these sources are believed to be reliable, the information has not been independently verified and is subject to material amendment, revision and updating, therefore no representation is made as to its accuracy or completeness. No reliance may be placed for any purpose whatsoever on the information, representations or opinions contained in this document nor shall it or any part of it form the basis of or act as an inducement to enter into any contract for any securities, and to the fullest extent permissible under UK law no liability is accepted or any such information, representations or opinions. The comments should not be construed as a recommendation of individual holdings or market sectors, but as an illustration of broader themes.